Accurate UK tax reporting is a cornerstone of client trust. But for wealth managers, financial advisers and platforms operating at scale, this process involves a complex interplay of data feeds, back-office systems, and operational controls that make it far from straightforward.

In this article, Financial Software Ltd (FSL) shine a spotlight on the intricate challenges wealth managers, investment platforms and financial advisers face in their day-to-day tax operations — from calculating capital gains and classifying income to account administration and reporting Excess Reportable Income.

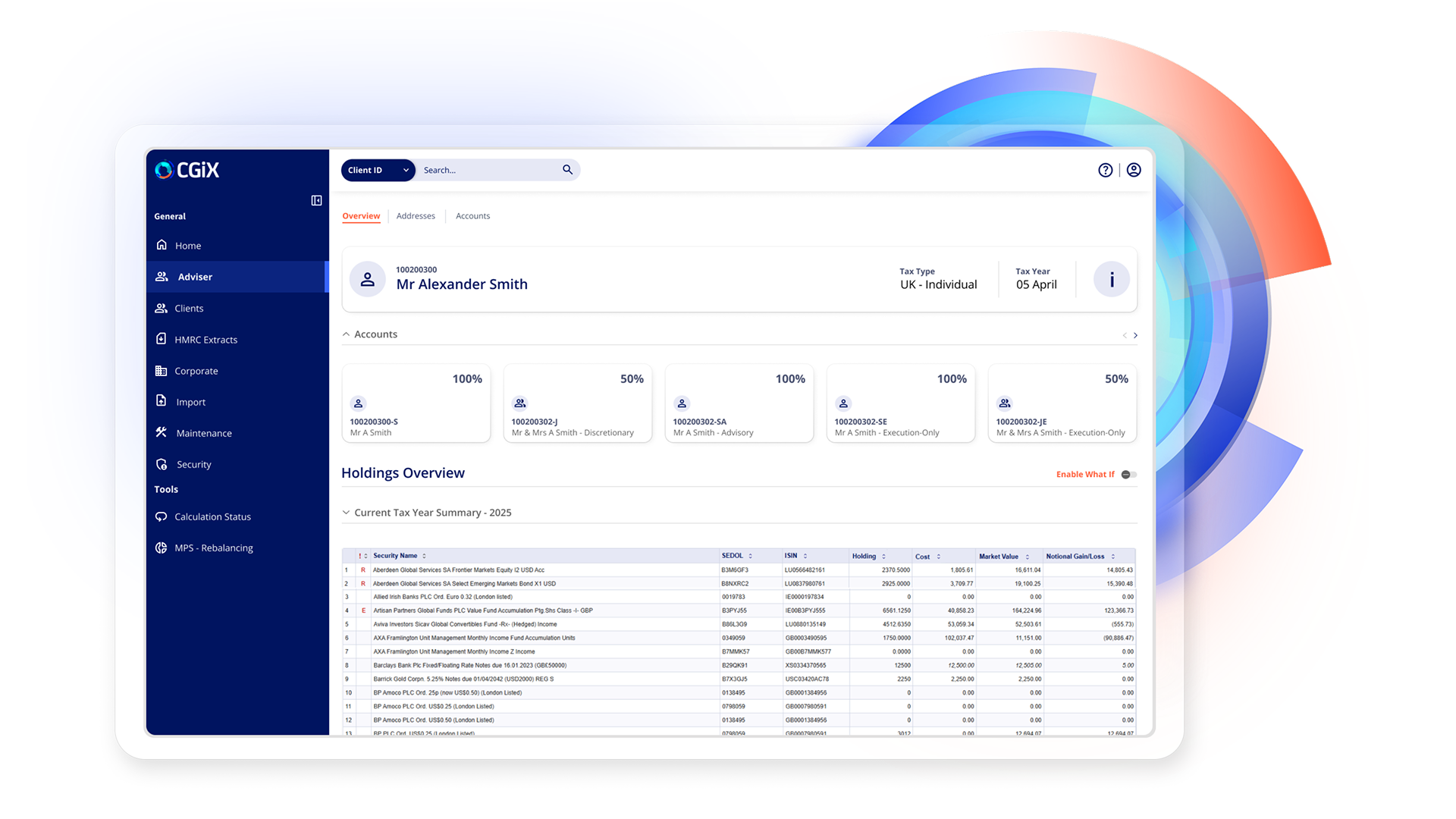

We’ll explore the operational and technological factors that contribute to the challenges that tax teams face with UK tax reporting, and how they could strengthen the quality and accuracy of their client-facing reporting with our award-winning CGiX software.

Topics covered:

- Excess Reportable Income: Delayed Processing and Back Dating

- Inaccurate and Estimated Book Costs

- CGT Mismatches: Spousal Transfers, Inter-Account Transfers and Share Matching Rules

- CGT Exemptions: Liable vs Exempt Assets

- Fund Classifications: OIECs, Unit Trusts, Bonds and ETFs

- Fund Conversions and Exchanges

- Missing Payments: Dividends and Unit Trusts

- Inaccurate Platform/Trail Commission Fees

- Trouble with Account Closures and Historic Tax Reports

Excess Reportable Income: Delayed Processing and Back Dating

Excess Reportable Income (ERI) is a niche and complex area of UK tax reporting that can be a real challenge for even the most skilled tax teams. There are many reasons teams struggle with ERI and, as trailblazers in raising industry awareness in the area, we’ve heard most of the challenges that advisers can face.

In this section, however, we will focus on the two challenges we see come up time and time again: issues with delayed ERI processing and challenges with back-dated ERI.

Delayed ERI processing and the impact on client reporting

UK investors are subject to tax on ERI if they hold the investment on the last day of the fund’s reporting period. However, ERI is only deemed to have been distributed to investors six months after the end of the fund’s reporting period. This ‘deemed disposal’ date is when ERI is treated as earned for UK tax purposes.

The six-month gap can create challenge for tax teams if an investor decides to dispose of their holding between the ex-dividend date and the pay date.

In fact, tax teams often find that:

- A client’s ERI is not accurately reflected in their annual tax summary.

- Incorrect capital gains tax (CGT) is applied on disposals occurring between the ex‑dividend date and the pay date.

This often results in tax teams manually producing ad-hoc tax packs to correct these issues, taking up valuable time and risking client confusion if the errors aren’t caught early enough.

With CGiX, ERI is recorded correctly and the relevant book costs are adjusted appropriately. CGiX ensures that the book cost adjustment is applied on the ex-dividend date and that the payment is recorded on the pay date.

Example scenario:

If an ERI payment has an ex-dividend date in the 2024/25 tax year, but a pay date in the subsequent tax year, CGiX applies the book cost adjustment for CGT in the 2024/25 tax year while reflecting the payment in the income report for the 2025/26 tax year.

Back-dated ERI and the impact on client reporting

Another common challenge is that many tax management systems struggle to handle back-dated ERI, leading to inaccurate annual tax summaries where a client has either wholly or partially sold their holding between the ex-dividend date and the pay date.

Often, tax teams are forced to implement time‑consuming reactive fixes, which may introduce further issues and delays if handled incorrectly.

In CGiX, any back-dated ERI entered into our software will automatically prompt the user to recalculate that portfolio. This recalculation updates CGT book‑cost positions to accurately reflect the back‑dated ERI payment.

Inaccurate and Estimated Book Costs

Book costs are vital for accurate CGT reporting. However, advisers are often frustrated by inaccurate, estimated or missing book costs which impact both their tax reporting and decision-making. This issue can be particularly troublesome when handling transfer in transactions.

Assets transferred into an account liable for CGT need to have a book cost reflecting the cost of the asset over the investor’s whole holding period. This should be carried over between providers to ensure accurate gain/loss figures. However, we often hear from tax teams that many systems/platforms don’t handle this scenario well.

When a transfer in occurs, tax teams are often forced to manually enter a book cost to allow CGT to be calculated on a portfolio. Where the book cost is left blank because it is yet unknown, systems will often default to a book cost of zero on a client’s final tax pack. This can inflate an investor’s gains and put them at risk of overpaying CGT.

With CGiX, holdings transferred in from another platform with an unconfirmed or zero book cost are automatically flagged as ‘estimated’ or ‘unknown’.

These flags ensure that all future transactions remain marked as ‘estimated’ or ‘unknown’ until the correct data is inputted and finalised. This informs the end-investor and their adviser that their final tax report is based on incomplete information, helping to reduce confusion and complaints.

CGT Mismatches: Spousal Transfers, Inter-Account Transfers and Share Matching Rules

UK share matching rules were designed to prevent tax avoidance, but their complexity introduces real operational challenges for tax teams looking to accurately report their clients’ CGT liabilities.

Without tax software that uses the correct logic, has the appropriate sensitivity to transaction dates, and holds accurate financial data, tax teams and advisers could find themselves at risk of producing inaccurate tax reports.

Spousal transfers and the 30-day rule

When a spouse or civil partner gifts an asset to their spouse or civil partner, the asset is transferred on a ‘no gain, no loss’ basis. This means the receiver treats the asset as if they’ve always held it, with the cost base carried over.

Trouble arises when the ‘gifter’ purchases more of the asset within a 30-day window. This event triggers share matching rules, with the outgoing spousal transfer transaction taking on the cost of the reacquisition.

This double impact can be too complex for many tax systems out there. Tax teams often tell us that their systems will not correctly apply share matching rules to the gifter’s transfer cost and, worse still, will not allow them to make any amendments.

This is because many other tax systems will calculate CGT on an account-level, leading to double taxation where the liability appears to lie with both investors.

CGiX will correctly apply the relevant rules to both the gifter and the receiver of the asset and ensure any chargeable events occurring within the 30-day window are reflected in your clients’ final tax packs.

Inter-account transfers and share matching rules

Transfers between accounts with the same beneficial owner should not incur a CGT liability as the transfer is viewed as neither a sale nor an acquisition for UK tax purposes. As a result, these transfers should be exempt from any share matching rules.

However, tax teams can run into trouble with these transfers as they are often flagged inaccurately in their systems.

From our countless conversations with wealth managers, private banks and financial advisers, we’ve heard that transactions such as these are usually flagged as ‘CGT exempt’ in their tax software. While this is true, the flag will often fail to stop their software from triggering share matching rules. This is usually because their software looks at transactions from an account-level only.

In CGiX, transfers such as these will always be labelled as ‘inter-account’. As a result, the transaction will not be considered liable for CGT, and any share matching rules will not be applied. This helps tax teams avoid manual workarounds and keep their tax reporting accurate.

CGT Exemptions: Liable vs Exempt Assets

Having the right information on securities is essential for accurate tax reporting. Many tax teams will use different data feeds for information on securities and manually check each to ensure the securities in their system are aligned and set up correctly. This can be a time-consuming and error-prone process that impacts final client-reporting.

Further, where data is inaccurate, wealth managers and financial advisers could find themselves guiding investors to exclude or include certain transactions because, according to their platform and data feeds, they would or would not be liable to CGT.

At FSL, we have a dedicated data team that integrates data from multiple vendors and applies their extensive financial expertise to ensure the accurate classification of assets within CGiX. This means that our clients have full confidence in the accuracy of their tax reporting before they hand over their annual summaries to an end-investor.

As part of our Specialist Tax & Data Consultancy service, we also offer asset classification reconciliation services which cross-references the CGT classification of assets before running tax packs. This proactive approach helps identify discrepancies early and keeps your tax reporting bullet-proof.

Fund Classifications: OIECs, Unit Trusts, Bonds and ETFs

Funds are an increasingly popular investment option that form part of many investors’ portfolios, but they aren’t always the easiest for tax teams to handle due to their complex characteristics and the rules that surround their distributions.

The 60% rule for funds

Where more than 60% of the assets in a fund are interest-bearing, HMRC states that any distribution or excess of reported income is treated as a payment of interest. For many tax management systems, keeping track of fund information and the type of distributions they give out can be a real nightmare.

We’ve heard of tax teams needing to check dividend types manually against a master spreadsheet that is maintained only through regular sanity checks. Issues begin when these checks fail or the master list isn’t properly maintained. This can cause errors to occur in a client’s tax pack – and that’s without mentioning how time-consuming and unscalable this work can be for teams managing a large number of complex portfolios.

In CGiX, offshore funds and unit trusts that allocate more than 60% of their assets to interest-bearing instruments will be classified as ‘Unit Trust and OEIC – Bonds’. This classification ensures that any payments will also be categorised as interest and taxed accordingly.

Conversely, offshore funds and unit trusts with less than 60% of their assets being interest-bearing are classified as ‘Unit Trusts and OEIC’. This ensures that any payments are instead classified as dividends with the appropriate tax rules being applied.

By having this system of classification, CGiX ensures that payments are properly and accurately presented in a client’s final tax certificate.

Distributions from ETFs

Tax management systems throughout the wealth management and financial services sector are reliant on data feeds. Many systems use multiple data feeds to gain accurate information about securities. However, not all these feeds are accurate, particularly when it comes to the classification of distributions received from ETFs.

At FSL, we have a dedicated data team that integrates data from multiple vendors and applies their extensive financial expertise to ensure the accurate classification of assets within CGiX. This means that our clients have full confidence in the accuracy of their tax reporting before they hand over their annual summaries to an end-investor.

Further, in CGiX, ETFs will be categorised on our Income Report based on the nature of the payment given to an investor. This will then come under the subheading ‘Overseas Exchange Traded Fund – Dividend’ or ‘Overseas Exchange Traded Fund – Interest’ so that there is no confusion on the tax treatment.

Fund Conversions and Exchanges

Conversions

Fund class conversions are not subject to CGT because they exchange shares in one class for shares of another class in the same fund. When a client informs a platform that they would like to perform a fund class conversion, many tax teams will find that their tax management systems aren’t able to handle this accurately or efficiently.

What we often hear from tax teams is that their systems will treat the conversion as liable to CGT which, in turn, triggers share matching rules against the transaction. This must then be manually corrected before it can impact client reporting – a time-consuming, unscalable and risky process.

With CGiX, conversion corporate actions are not treated as CGT-liable events and can be applied to the relevant client portfolios with ease.

Our software will move shares from a parent asset to a resultant asset, all while maintaining the original CGT information. We will also automatically apply the correct Income Group 1, Group 2 or Equalisation transaction to the parent asset and resultant asset.

Exchanges

Fund class exchanges are a similarly tricky area to conversions for tax teams but for different reasons.

From our conversations with wealth managers, platforms, private banks and financial advisers, we hear that tax teams will often complain that when they attempt to perform a fund switch on behalf of a client, a CGT liability will be generated on a client’s account because their system will actually dispose of the investor’s units.

In CGiX, tax teams can record fund exchanges without treating them as disposals. This ensures that asset transitions are accurately tracked while maintaining continuity in CGT calculations.

Missing Payments: Dividends and Unit Trusts

Missing payments

Tax teams told us that they can struggle to keep track of payments depending on what data feeds they choose to use. They often find that payment events are missed after the release of their annual tax summaries, leading to lengthy and error-prone remediation work to determine which investors need an updated tax summary.

With CGiX, any discrepancies in the current holdings between your data feeds and our software will be detailed in our automatically produced Reconciliation Report. This report is accessible at both the system level and the individual client level, and it details breaks at the ‘Shares’ and ‘Expense’ level.

Any variances resulting from the application of ERI, Income Group 1, Income Group 2 or equalisation payments in CGiX, which have not been reflected on the platform, will be highlighted in the Reconciliation Report.

Missing payments and the classification of Group 1 and 2 units

Unit trusts tend to have fixed dates on which they pay distributions. They tend to also have fixed dates which determine whether an investor will be eligible to receive these distributions.

Investors will be entitled to the unit trust’s income in a given distribution period if they hold units at the unit trust’s dividend record date (the day before its ex-dividend date). This means that even if the unit trust’s income arose before an investor had purchased their units, they will still be entitled to an equal proportion of this income so long as they hold units at this date.

However, to ensure fairness, unit trusts will operate an equalisation scheme. This splits into two groups, as determined by the dividend record date: those who bought units before the distribution period and those who bought units during the distribution period.

Units bought before the distribution period are referred to as Group 1 units, and units bought during are referred to as Group 2 units. Investors who hold Group 2 units will have been required to pay an extra amount to purchase their units, on top of the standard price. This extra amount is the amount of income earned by the unit trust to date since its last distribution date.

When the unit trust’s next distribution is paid, the investor holding Group 2 units will receive the same amount of cash per unit as the investor with Group 1 units, but part of their cash will be a refund of the extra amount they paid for their units. This is known as an equalisation payment.

With many tax reporting solutions, this payment is misclassified. The misclassification then often requires tax teams to manually input how many units would be classified as Group 1 and how many would be classified as Group 2 – a time-consuming and error-prone process.

CGiX automatically applies the correct Group 1 or Group 2 designation to units based on when they were purchased within each account period.

Group 1 will be applied to units held for the full account period and Group 2 will be applied to units purchased outside the account period. When both new and existing units are present, CGiX will ensure the correct proportional application of Group 1 and Group 2 for the investor.

If an investor holds Group 2 units, CGiX will also take the equalisation payment into account when calculating their tax liability.

Inaccurate Platform/Trail Commission Fees

A platform/trail commission is a rebate or fee paid to investors. It usually originates from the annual management charge paid by the fund to the fund manager and is subject to income tax if distributed to a taxable account.

Many tax teams find that these commissions can trigger a tax charge to be noted in non-taxable accounts, like ISA or SIPPs, on their platform. When this happens and the fund are distributed, this often results in the debit balances of their clients’ accounts to be inaccurate.

CGiX caters for fees and trail commissions banked against CGT accounts on behalf of investment platforms. It reports these transactions separately as subject to income tax within an investor’s Consolidated Tax Certificate report. By default, these transactions are logged as ‘Commission Rebate’ in CGiX but we give our users the flexibility to rename this manually, should they wish.

Trouble with Account Closures and Historic Tax Reports

When an account goes through a close-down process, an investor will lose access to their investment account and usually no longer be able to access the platform’s documents section to view their tax packs.

Tax teams have found that when a customer closes their account between tax pack releases, they are unfortunately unable to access their latest tax pack once it’s been released. This can lead to queries and complaints, particularly around tax year-end, when former customers frantically try to access their latest tax pack.

Generally, for tax teams this means each closed account must be manually re-opened, run and sanity checked, taking up time at an already busy time of year.

In CGiX, when an account is closed, all linked data – including transaction information – will become read-only. However, reports remain accessible so that users can still view historical transactions and calculations before closure. This ensures data integrity whilst still maintaining access to essential client records and allows tax packs to be run without a separate operational tax pack run flow just for closures.

Got a tax challenge not included here? Get in touch to see how we could help.

- Introduction

- Excess Reportable Income: Delayed Processing and Back Dating

- Inaccurate and Estimated Book Costs

- CGT Mismatches: Spousal Transfers, Inter-Account Transfers and Share Matching Rules

- CGT Exemptions: Liable vs Exempt Assets

- Fund Classifications: OIECs, Unit Trusts, Bonds and ETFs

- Fund Conversions and Exchanges

- Missing Payments: Dividends and Unit Trusts

- Inaccurate Platform/Trail Commission Fees

- Trouble with Account Closures and Historic Tax Reports